Devesh Shah

Happy new year to all of you. May peace come to your home, the earth, the stars and all living things. I am very happy to announce that I recently published a children’s stage play book.

Growing up in Mumbai, India, I studied in schools where theater and theater were an important part of education. At that time, many of our school plays were drawn from English literature. A few years ago, I was asked to translate nine of his plays written in my native language, Gujarati, into English. Acclaimed playwright Prakash Lala wanted to reach young children around the world with his stories. The average 10- to 12-year-old child in India has a different education than a child in America. Families, grandparents, domestic helpers, and even neighbors play a much bigger role in raising children than we see in our society here. and recently published a book on Amazon.Look for the title “”nine children’s games‘I hope you do Read it and share it with your friends and family.

Long-term TIPS bond prices now provide a margin of safety. I’m buying

I’m buying long-term (10-30 year maturity) TIPS bonds this month. I would like to share why.

In this article, I write about why Treasury Inflation Protected Securities (TIPS) are finally ready to serve their purpose of protecting against inflation. TIPS currently have a high enough real yield to make a good investment. Over the past few weeks, he has invested over 25% of his portfolio in his TIPS, from single-digit percentage allocations to TIPS.

Readers who want to understand the asset allocation rationale for having TIPS in a portfolio, TIPS terminology and bond calculations, or the difference between TIPS and Series I bonds should first read my other three articles on inflation protection. You may want to read MFO in last 12 months:

February 2022: Inflation protection considerations

August 2022: I hope I can give you some tips to beat inflation

October 2022: Series I Bonds: A Ray of Hope

Why am I so focused on TIPS? Aren’t they a big disappointment?

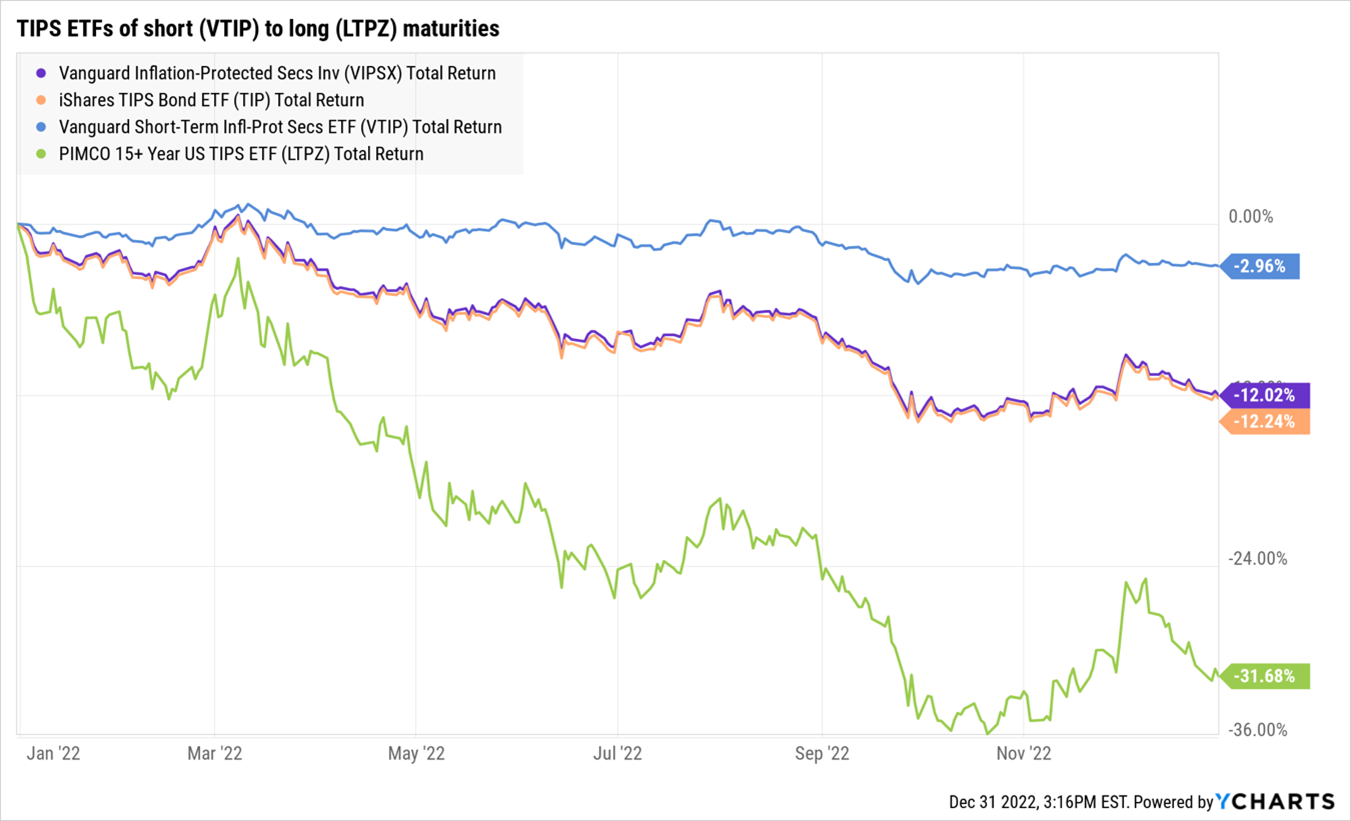

- Viscerally, I feel the inflation monster everywhere. None of the services, items, or experiences I am looking to purchase are priced the same or cheaper than they were a few years ago. It is a natural instinct to protect purchasing power. TIPS is the only direct investment product that has a direct link to inflation. They are US government credit risk and are priced in US dollars. 2022 should have been the year of TIPS. It wasn’t. In my previous article, I explained why TIPS disappoints, and it did. The TIPS ETF’s total return was down 3% for the shortest maturity and negative 32% for the longest.

- Even though inflation was burning in 2022, the TIPS entry price was wrong: TIPS was too high this year. Bonds are priced much higher now.

- I was worried that controlling inflation would be easier said than done, so I wanted to significantly increase my exposure to TIPS. The Fed’s resolve could be shaken when things get tough, including high US government interest rates, corporate debt repayments, financial disasters, and recessions.

- There are also growing voices that the 2% inflation target is unnecessary. In the future, will we live in a world where CPI is 3-4%, instead of 2% in the past? will be

- If inflation becomes an inherent feature, fixed coupon bonds will suffer losses. On the other hand, TIPS bonds hold up better, especially given their current pricing.

What are the changes to TIPS from the beginning to the end of 2022?

- TIPS trading based on real yield. To understand real yields, read his MFO article from August. TIPS buyer gets real yield at time of purchase + her future CPI.

- At this time last year, investors paid the US Treasury to hold TIPS. The real yield is negative. But now investors are being paid at a pretty positive real yield to hold her TIPS.

| TIPS bond maturity | December 31, 2021 | December 31, 2022 | Change |

| 5 years | -1.61% | 1.66% | 3.27% |

| 10 years | -1.04% | 1.58% | 2.62% |

| 30 years | -0.44% | 1.67% | 2.11% |

- TIPS real yields have been revised up and TIPS bond prices have been revised down enough this year to make an interesting investment. TIPS is finally ready to meet its policy goal of protecting investors from inflation. The chart below shows that real yields have been revised upwards from 2021 lows compared to nearly 20 years of history. Yields today are competitive.

Isn’t it true that yields on fixed-rate government bonds have also risen? Why not invest in US Treasuries? Why bother investing in TIPS?

- Yields (or interest rates) are much higher everywhere. Let’s take a look at last year’s fixed-coupon government bond yields.

| term bond | December 31, 2021 | December 31, 2022 |

| 5 years | 1.37% | 3.99% |

| 10 years | 1.63% | 3.88% |

| 30 years | 2.01% | 3.97% |

- Yields on fixed-coupon government bonds are also significantly better than they were a year ago. The same is true for municipal bond yields. However, only his TIPS of the US government are exposed to rising inflation.

- Then there is the tax issue. As a private investor in New York, if you invest through a taxable account, you may be better off holding New York municipal bonds than fixed-rate US government bonds.

- I prefer TIPS over both fixed US Treasuries and Muniz because if the Federal Reserve loses control of inflation, TIPS will be the only one of the three bonds that will claim my purchasing power. you know where my head is I hope they don’t mess up, but if they do, I don’t want to go with them.

What could go wrong if I buy TIPS now?

- I may be early If the Federal Reserve continues to raise rates and US fixed bond yields continue to rise, so will TIPS real yields. TIPS bonds then fall. The question is: “Are you ready to increase your allocation to fixed income and TIPS?” I believe so.

- Inflation may collapse. In that case, my spending will slowly increase as well. Also, the Federal Reserve could cut interest rates, which could actually support all kinds of longer-term bonds because of the duration risk.

- US government credit can be more risky. I’ll assign that as the unlikely scenario for now.

What assets am I selling to buy TIPS now? What am I rebalancing from?

- This is a really good question. In 2022 all assets were down. You have to starve Peter to feed Paul. I have lightened my stock across the board and am using that cash to buy his TIPS.

- We are far more confident about the current margin of safety for TIPS bonds than the margin of safety for all types of equities, including US value stocks. Therefore, I have reduced my exposure to US value stocks to buy his TIPS.

What are the different scenarios for buying 30-year TIPS now?

- Base Case: The bond market now believes the CPI will hover at 2.3% over 30 years, with a real yield of 1.65%. This means the yield to maturity is in the 3.95% zone. Assign this with a probability of 50%.

- Bear Case: Real Yields on Long-Term Interest Rates If inflation is high and the Federal Reserve continues to raise rates, the TIPS will be between 1.65% and 2.5%. TIPS bonds lose 18-20% in market value, but end up yielding close to 5% over the long term. Current Real Yield (1.65%) + CPI (3-4%). Allocate this to the 15% scenario. It will hurt at first, but in the end it will help.

- BullH is The Case: Real yields have fallen from 1.65% today to 1%, and CPI averages 2%. This lower yield could result in an 18% increase in price and CPI. Assign it a probability of 35%. You can see the mark-to-market gain of the TIPS price. At that point, you’ll have to assess my views on inflation.

I’m sure there are more ominous bear scenarios and more challenging bull scenarios, but none of these are for investors unwilling to embrace significant volatility.

Why not buy and hold your entire bond portfolio?

- For the majority of investors, perhaps 97%, the Total Bond portfolio will be fine. No need to do more than that. Intellectual honesty is important here. If you can’t stand losing money on your assets, or you don’t want to increase your quota when your investment goes against you, you shouldn’t take aggressive risks. In those cases, benchmarking the portfolio to a simple formula is all I’ve done so far.

- But I believe that diving deep into the market and all the analysis that comes with it is more than just intellectual curiosity. I’m here. This last bit indicates that it’s okay to buy TIPS now. Every morning I find TIPS bonds dropping in price and add them to my portfolio.

The conclusion is

It is up to each investor whether they need to own TIPS or just the entire bond portfolio. Whenever a person is in danger, an element of positive risk is always introduced. We want to secure a real yield of 1.65% and are interested in receiving CPI, so we are investing in TIPS. Furthermore, I worry that the CPI will not fall as smoothly as the bond market hopes. For those who want to study TIPS and are worried about inflation, it would be a waste not to miss this opportunity.

For investors interested in investing in long-term TIPS, the best option is probably PIMCO 15+ Years US Tips ETF (LTPZ) costs 0.20% and has a shelf life of just over 20 years, compared to 6 years for its peers.