Updated January 27, 2023 Nathan Parsh

Investors looking for quality dividend growth stocks should look first and foremost to Dividend Aristocrats. The Dividend Aristocrats are an exclusive list of 68 stocks in the S&P 500 Index with over 25 years of consecutive dividend increases.

Dividend Aristocrats are an elite group of dividend growth stocks. For this reason, we have compiled a complete list of all 68 Dividend Aristocrats.

Click the link below to download a free copy of the Dividend Aristocrats list and key metrics such as dividend yields and price/earnings ratios.

T. Rowe Price Group (TROW) is on the Dividend Aristocrat List and is one of only seven Dividend Aristocrats in the financial industry. It has increased its dividend for 35 consecutive years, including an impressive 20% increase on February 9, 2021. T. Rowe Price has a strong brand, profitable business and future growth potential.

The stock’s dividend yield is 4.2%, above the broader S&P 500 index’s average dividend yield of ~1.6%. All in all, T. Rowe Price stock has many of the qualities that dividend growth investors typically look for.

Business overview

T. Rowe Price was founded in 1937 by Thomas Rowe Price, Jr. In the 80 years since, T. Rowe Price has grown to become one of the largest financial services providers in the United States. Today, the company has a market capitalization of approximately $26 billion and manages approximately $1.3 trillion in assets at the time of this writing.

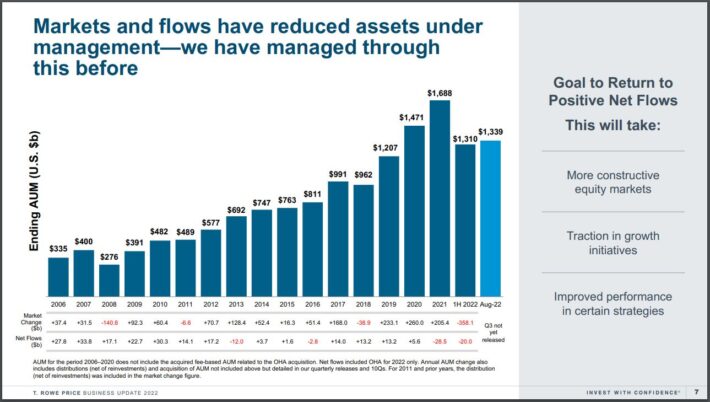

Source: Presentation for investors

The company offers mutual funds, advisory services and individually managed accounts for individuals, institutional investors, retirement plans and financial intermediaries.

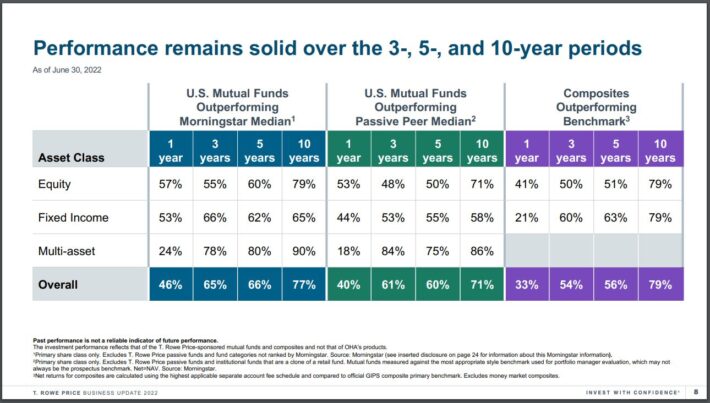

T. Rowe Price has a diverse customer base in terms of assets and customer types. The company has an impressive record of investment performance over the last five and ten years.

Source: Presentation for investors

This is a difficult situation for asset managers. Some investors are fed up with rising transaction costs and annual fees. The advent of low-cost exchange-traded funds (ETFs) has successfully pulled client wealth away from high-fee traditional mutual funds. This allows brokers to keep their clients’ wealth by lowering their fees and commissions.

However, T. Rowe Price’s stock continues to perform well and the company has significant growth potential over the next few years.

growth outlook

T. Rowe Price has many catalysts for future growth. The first catalyst is Trenimon’s amount of assets under management, even after the recent market decline.

Fourth quarter assets under management (AUM) decreased 12.6% compared to the fourth quarter of 2021 to $1.27 trillion. This was driven by net customer outflows of $17.1 billion, net distributions not reinvested of $2.5 billion, and customer transfers of $2.1 billion. billion, and market depreciation.

Net revenues in the most recent quarter were down 22.4% to $1.52 billion. His adjusted earnings per share were $1.74, up from $3.17 a year ago, but he beat analyst expectations by $0.03.

Full-year revenue declined 15.4% to $6.5 billion, with adjusted earnings per share of $8.02, down from $12.75 in 2021.

The share buyback is also part of the company’s earnings per share growth plan. T. Rowe Price has reduced its weighted average number of diluted shares by 1.7% in 2022. In addition, fewer shares outstanding means more earnings per share, thus increasing the value of each share.

Competitive Advantage and Recession Performance

T. Rowe Price’s competitive advantage comes from its brand recognition and expertise. The company has a strong reputation in the financial services industry. This helps generate commissions, which are an important driver of revenue. We have built this reputation through the excellent performance of our mutual funds.

T. Rowe Price believes its employees are its most valuable asset. There are good reasons for this. It is important for asset managers to have qualified professionals and retain top talent. The focus on building a strong brand gives the company a competitive advantage, primarily due to its ability to retain existing customers and acquire new customers.

T. Rowe Price did not perform well during the Great Recession.

- Earnings per share of $2.40 in 2007

- Earnings per share of $1.82 in 2008 (down 24%)

- Earnings per share of $1.65 in 2009 (down 9%)

- 2010 earnings per share of $2.53 (up 53%)

As expected, T. Rowe Price experienced a sharp decline in earnings per share in 2008 and 2009. When the stock market falls, stock investors typically withdraw their funds to raise cash.

Luckily, the company remained profitable during the recession and was able to raise its dividend each year. And T. Rowe’s price quickly recovered in the aftermath of the Great Recession. Earnings he increased significantly in 2010 and hit a record high in 2011.

Also worth noting is the company’s strong balance sheet. As of the most recent quarter, T. Rowe had $1.8 billion in cash, in total assets he held $11.6 (35% of which was invested), total liabilities were his $1.1 billion, and long-term debt was Zero.

Valuation and Expected Return

T. Rowe Price expects 2023 adjusted earnings per share to be $7.25. Using the recent stock price of $114, the price/earnings ratio is 15.7. The 2028 target price/earnings ratio is 14. If the stock reverts to fair value estimates, the total return would decrease by 2.3% annually over the next five years.

The company has a strong brand and has seen fairly steady profitability and earnings growth, but T. Rowe Price’s stock is overvalued. Combined with a huge number of assets under management and share buybacks, he sees earnings per share growing at a rate of 3% annually through 2028.

So the total return will be:

- 3% profit growth

- 4.2% dividend yield

- -2.3% multiple shrinkage

T. Rowe Price is expected to return 4.9% annually through 2028. T. Rowe Price is a particularly attractive stock for dividend increases. The company has been increasing its dividend for over 36 years in a row, including his 11.1% increase in 2022. Also, this year’s expected payout ratio is below 66% for him, so the dividend is pretty safe.

final thoughts

Investors scanning the financial sector for dividend stocks may naturally land on the big banks. But the only bank stock on the Dividend Aristocrats list is People’s United Financial (PBCT).

In fact, most dividend aristocrats from the financial sector come from the insurance and investment management industries. This speaks to the stability of their business model.

T. Rowe Price is an industry leader and needs to keep increasing its dividend every year. The focus on lowering fees will continue to be a headwind for the industry. T. Rowe Price stocks receive a Hold Rating due to expected returns.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe.

If you’re looking for stocks with unique dividend characteristics, consider the Sure Dividend database below.

Thank you for reading this article. Send any feedback, corrections, or questions to support@suredividend.com.