Updated January 24, 2023 Nikolaos Sismanis

Nucor Corporation (NUE) is the largest steel producer in North America. Despite operating in a volatile and notoriously volatile raw materials sector, Nucor is also a very stable dividend growth stock. The company has increased its annual dividend for 50 consecutive years and is eligible to be a member of the Dividend Aristocrats list.

Dividend Aristocrats are relatively rare in the S&P 500, with a long history of increasing their dividends year after year, even during recessions. With that in mind, here’s a list of all 65 Dividend Aristocrats, along with their price/earnings ratios and dividend yields.

Following its recent dividend increase, the company also joins the elite group of dividend kings. Only 48 companies qualify to be members of the Dividends Kings universe (i.e. have increased their dividends for 50+ years).

Click the link below to download an Excel spreadsheet containing the full list of Dividend Aristocrats.

Nucor’s dividend consistency allows Nucor to stand out within its sector and among its constituent elite groups. Currently, he has seven Dividend Aristocrats and only three Dividend Kings in the Materials Division.

Steel is a particularly challenging industry due to the cyclical nature of its business model, making Nucor’s consecutive annual dividend increases even more impressive.

In this article, we’ll analyze Nucor’s business model, growth prospects, and valuation to help you decide if you should buy the stock now.

Business overview

After decades of growth, Nucor is the largest steel producer in North America. The company is headquartered in Charlotte, North Carolina and has a market cap of $39.5 billion.

Nucor has not always been a leader in the steelmaking industry. The company has a long and complex corporate history that can be traced back to its founder, Ransom E. Olds (the father of the Oldsmobile automobile). Olds left his own car company over disagreements with his shareholders and founded his company REO Motors. This eventually became Nucor’s first predecessor, Nuclear Corporation of America.

The company currently operates in three segments: Steel Mills (the largest segment by revenue), Steel Products, and Raw Materials.

Source: Presentation for investors

Nucor manufactures many types of materials including steel plates, bars, structural structures, steel plates, downstream products and raw materials. The bulk of the company’s production is, as it has been for many years, a combination of steel plates and bars.

Nucor’s focus on low-cost production has resulted in long-term success. This not only allows us to remain profitable during downturns, but also allows us to generate significant operating leverage during upturns. In addition, we have worked to expand our product offerings into new markets and maintain and extend our market leadership in our existing channels. Over time, these principles have served Nucor very well. As such, Nucor is now the largest producer in North America.

growth outlook

The past few years have been volatile for Nucor and its competitors around the world. Steel prices are highly volatile, largely driven by oversupply from international markets, especially from China.

However, the recent outlook for the industry is very good. China’s Q4 2022 GDP and December industrial production both grew better than market expectations, but the end of the zero-Covid policy and considerable initiatives to stimulate construction activity have pushed the real estate sector down. will strengthen, increasing demand for steel.

Revenue in the third quarter was $10.5 billion, up 1.8% year-over-year, despite an 11% decline in shipments to external customers over the same period. This is because the average selling price per tonne has increased by 14% year-on-year.

Earnings per share for the third quarter were $6.50, compared with $7.28 per share in the year-ago quarter.

Nucor is expected to report EPS close to $29.52 for the full 2022, compared to $23.44 per diluted share in 2021.

It’s worth noting that Nucor’s 2022 EPS is expected to grow further from its already record levels in 2021, which came from much lower bases in 2020 and 2019.

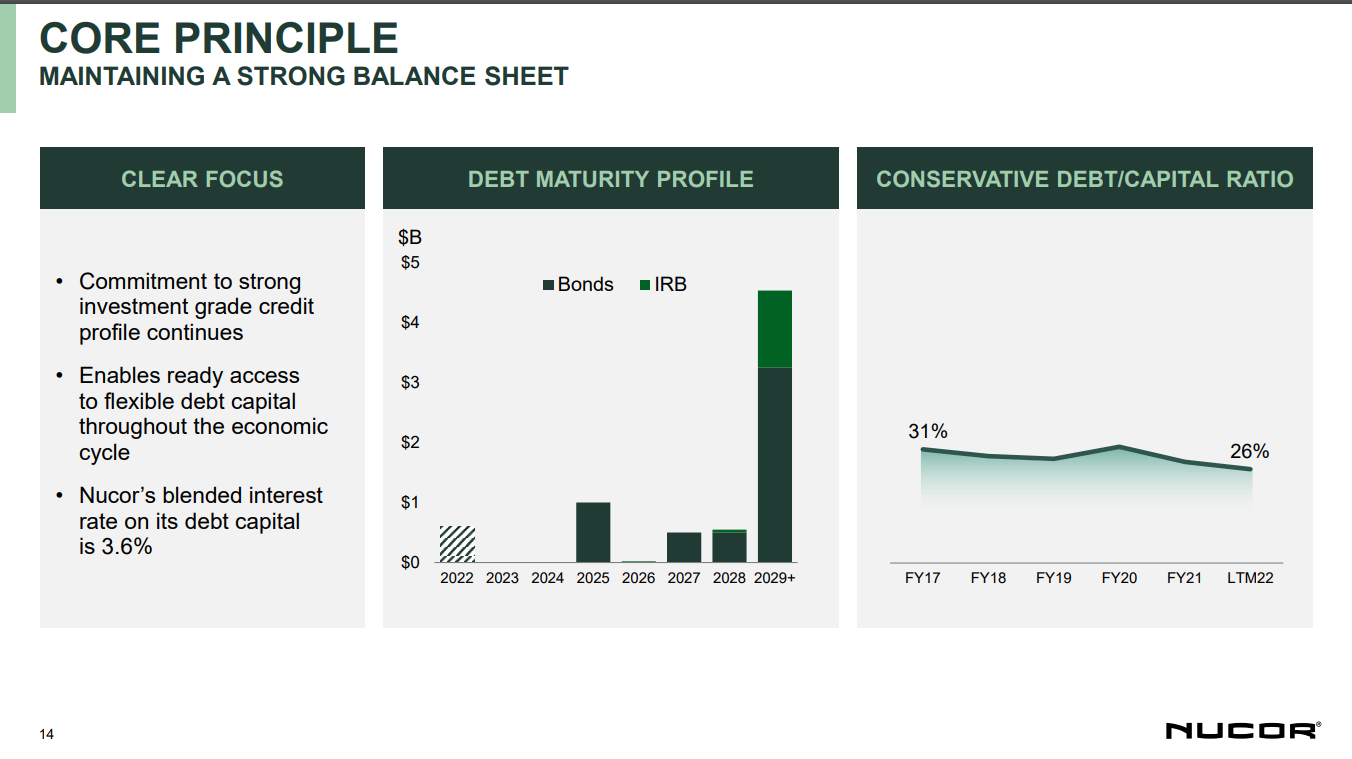

Nucor’s unique ability to increase dividends as a commodity producer for 50 years is largely due to its position as a low-cost producer and its propensity to maintain a healthy balance sheet.

Source: Presentation for investors

This has allowed Nucor to remain profitable and increase dividends throughout all economic cycles, but so many high-cost commodity producers will not stand the test of time.

Investors can get an idea of how fast Nucor could grow in the future by looking at Nucor’s historical growth rates over past cycles. Between 2001 and 2016, Nucor doubled adjusted earnings per share to 13%, but 2016 was still a weak year for the steelmaker.

We believe Nucor is likely to deliver adjusted earnings per share growth of approximately 3.7% from this point forward, although net earnings growth has been bumpy thanks to Nucor’s presence in the cyclical materials sector. will be Nucor’s near-term earnings potential is near the top, given the tremendous progress and recovery in earnings seen over the past two years.

Longer term, the long-term growth prospects for Nucor’s market are generally positive. Nucor’s diversification with respect to end markets is not only a key driver of growth, but also provides relative safety in the event of a recession. This allows the company to outperform other steel makers during recessions.

Overall, assuming earnings power of $5.00 in 2022, annual earnings per share growth is expected to be 3.7% over the next five years. of business.

Competitive Advantage and Recession Performance

Nucor is a manufacturer and distributor of raw materials and steel. The company is therefore a “commodity business” and its single biggest differentiator from its competitors is price.

Warren Buffett said of the commodity business:

“Stocks in companies that sell commodities-like products should bear the warning label ‘Competition can be a danger to human wealth.’” – Warren Buffett

The commodities business is certainly not the most defensive business, thanks to its cyclicality. You can see this in his Nucor performance during the 2007-2009 financial crisis.

- 2007 adjusted earnings per share: $4.98

- 2008 adjusted earnings per share: $6.01

- 2009 Adjusted Earnings Per Share: Net Loss ($0.94)

- 2010 adjusted earnings per share: $0.42

- 2011 adjusted earnings per share: $2.45

Nucor’s earnings per share were significantly reduced by the financial crisis. The company is one of the few dividend aristocrats whose earnings have actually turned negative during this tumultuous time. Nucor continues to steadily increase its dividend payout, but earnings only recently caught up to pre-recession levels.

With all this in mind, Nucor should not be viewed as a defensive investment. Investors should expect companies to suffer during recessions. Moreover, with steel being used as a bargaining chip internationally in political bargaining, investors should be aware that a company’s fate is tied not only to their own actions, but potentially to outside forces as well. I have.

Valuation and Expected Return

Nucor is expected to report adjusted earnings per share of approximately $29.52 in fiscal 2022, but assumes a normalized earnings per share force of $5.00 to smooth the cyclicality of results doing. This gives a price/earnings ratio of approximately 30.8, well above the fair value estimate of 12.0. We maintain a more cautious stance on steelmakers than on the general market, partly due to volatility in commodity prices.

You see fair value at 12 times earnings. I mean, his Nucor today is pretty overrated. The cyclical nature of Nucor’s business model means that changing which year’s earnings are used can have a significant impact on the company’s valuation. In fact, his earnings per share in 2018 represented that cycle’s high, which made the stock look cheap at the time.

Given this, using dividend yield as a valuation metric helps signal what investors understand about valuation. The current yield is 1.3%, well below the average dividend yield of around 3%.

Annual EPS growth of 3.7% is likely to be significantly offset by Nucor’s valuation multiple compression, resulting in a negative 10.4% annual total return over the next few years. Tighter valuations could result in annual returns of -17.2%. Yield is low at 1.3%.

Nucor’s dividend track record is very impressive. More recently, it has increased its dividend for 50 consecutive years. We have paid quarterly dividends for 199 consecutive times. That said, dividend growth has lagged on average over the past decade, with a recent increase of just 2%.

Nucor is recession-susceptible and investors should consider the impact of a recession before purchasing shares. Additionally, given the high valuation, we believe investors should wait for a better price.

final thoughts

Following Nucor’s status as Dividend Aristocrat and its recent dividend increase as Dividend King, it stands out in a highly volatile materials sector. Several raw materials businesses have a track record of doubling adjusted earnings per share over decades.

Nucor has a long history of annual dividend increases, a strong industry position and a healthy balance sheet, but Nucor currently has a lower dividend yield than the S&P 500 Index.

Overall, this stock does not deserve a buy recommendation at its current price. And the company will be hit hard by the recession. Investors looking for raw material exposure are advised to wait for a better opportunity to acquire Nucor shares.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe.

If you’re looking for stocks with unique dividend characteristics, consider the Sure Dividend database below.

Thank you for reading this article. Send any feedback, corrections, or questions to support@suredividend.com.