Updated February 13, 2023 Samuel Smith

Johnson & Johnson (JNJ) is a company that many investors are probably familiar with. J&J has been in business for over 130 years and has increased its dividend for 60 consecutive years. He has one of the longest and most impressive histories among dividend growth stocks.

J&J is a longtime member of the Dividend Aristocrats. Click the link below to view the full downloadable list of all 68 Dividend Aristocrats (along with key financial metrics such as dividend yield and price/earnings ratio).

Johnson & Johnson is not only a dividend aristocrat, it is also a dividend king. Dividend Kings is an even more exclusive group of stocks with over 50 consecutive years of dividend increases. Only 48 companies achieved this achievement.

J&J has all the qualities you want in a high dividend growth stock. With a dividend yield above the S&P 500 average, the company has long-term growth potential underpinned by a strong brand and profitable business model.

This article describes a typical dividend aristocrat who is Johnson & Johnson.

Business overview

J&J is one of the world’s largest companies, but it started from very humble beginnings. Founded in 1886 by his three brothers Robert, James and Edward Johnson. In 1888, the three brothers published a health care manuscript entitled “Modern Methods of Antiseptic Wound Treatment”. It quickly became the leading standard in antiseptic surgical technique.

Over the decades that followed, the company steadily introduced new products to the market. Soon, the company became a leading manufacturer of several healthcare categories, including baby his powder, sanitary napkins and dental floss.

Today, J&J is a global healthcare giant. It has a market capitalization of $424 billion. J&J is a megacap stock, a term used to describe stocks with a market cap of over $200 billion. A list of MegaCap stocks can be found here.

J&J currently manufactures and markets healthcare products through three main segments:

- pharmaceuticals

- Medical equipment

- consumer health products

The company has a diversified business model and strong brands across three main business segments. You can see the performance breakdown for each segment in the image below.

Source: Presentation for investors

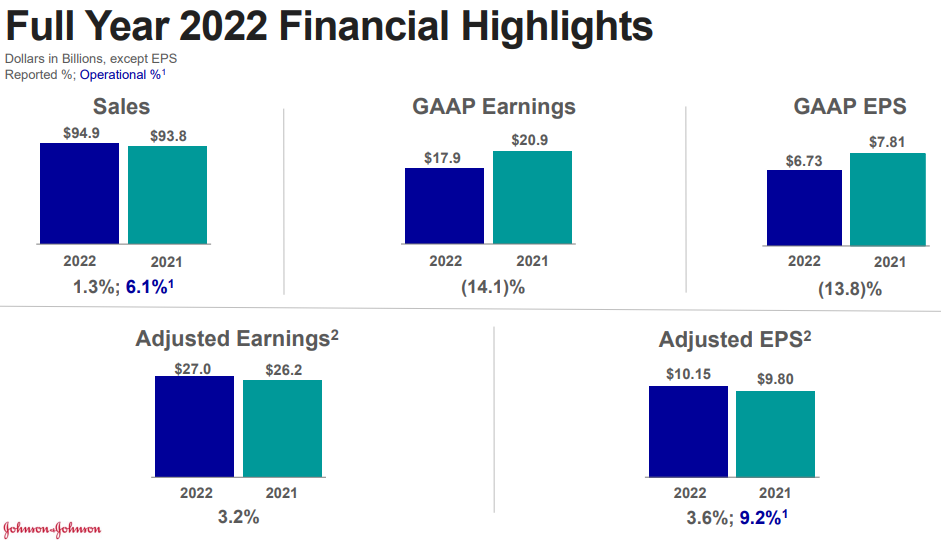

On January 24, 2023, Johnson & Johnson announced fourth quarter and full year earnings results for the period ending December 31, 2022. Earnings for the quarter fell 4.4% to $23.7 billion, $200 million less than expected. Adjusted earnings per share were $2.35, up from $2.13 last year and beating expectations by $0.11. Revenue in 2022 increased 1.3% to $94.9 billion. Adjusted earnings per share totaled $10.15, compared with $9.80 in the prior year. Unfavorable currency and lower Covid-19 vaccine sales impacted results. Excluding these factors, sales increased by 4.6%.

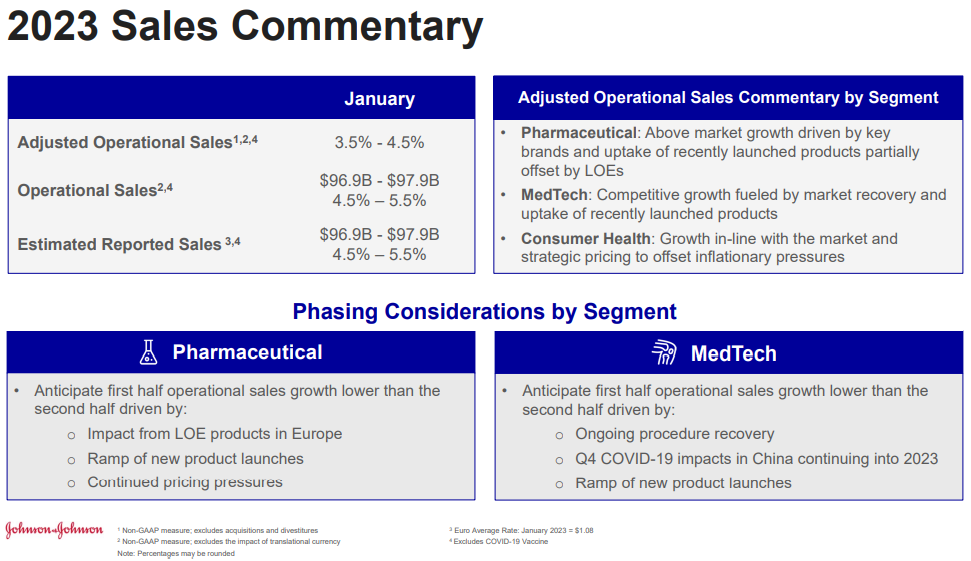

Johnson & Johnson also released guidance for 2023. The company expects full-year revenues of $96.9 billion to $97.9 billion and adjusted earnings per share of $10.45 to $10.65. At the midpoint, they grow at 2.6% and 3.9%, respectively.

Source: Presentation for investors

growth outlook

Pharmaceuticals revenues declined 7.4% on a reported basis in the latest quarter (down 2.5% at constant currency). This was primarily due to a sharp decline in sales of Covid-19 vaccines. As a result, infections decreased by 36%. Oncology increased 3.9% as Darzalex, which treats multiple myeloma, continues to gain market share. Imbruvica, which treats lymphoma, once again led the market, but lost due to competitive pressure. Immunopathies declined 5.4% (-1.8% excluding currency) as increased market share for STELARA, which treats immune-mediated inflammatory diseases, was offset by unfavorable patient mix and higher rebates. Consumer revenues increased 1.0% (6.4% at constant currency) driven by strong OTC and slightly higher Skin Health & Beauty. All businesses were down during this period. MedTech declined 1.2% in the fourth quarter (up 4.9% at constant currency). This was driven by strength in intervention solutions offset by weakness in all other areas.

Acquisitions are another growth catalyst for the company. J&J makes acquisitions, both large and small, to accelerate its growth. From 2016 to 2018, Johnson & Johnson spent over $40 billion on acquisitions. The biggest of which was his $30 billion acquisition of his independent R&D company, Actelion. Actelion’s R&D focuses on rare diseases with significant unmet need, such as pulmonary arterial hypertension.

Johnson & Johnson’s large business platform and global reach give the company a lasting competitive advantage that has fueled its growth over the past decades.

The company is also in the midst of a major transformation of its business model. Announced on November 12, 2021, Johnson & Johnson plans to spin off its consumer health business into a separate entity. While this business has been the face of the company for years, pharmaceuticals and medical devices contribute far more to revenue and bottom line each year.

We expect the transaction, which is expected to close in mid-2023, to unlock value for shareholders.

Competitive Advantage and Recession Performancee

Johnson & Johnson’s most important competitive advantage is innovation, which has driven the company’s incredible growth over the past 130 years. Its strong cash flow allows it to spend a lot of money on research and development. Research and development is important for healthcare companies as it provides product innovation.

R&D is needed to stay ahead of the dreaded “patent cliff”. Blockbuster drugs can quickly deteriorate due to patent expiring as a large amount of competition enters the market. J&J’s aggressive R&D investments will lead to product innovation and a strong drug pipeline that will help generate growth in the years to come.

And J&J’s strong balance sheet gives it a competitive edge. The company, along with Microsoft (MSFT), is one of only two US companies to receive a ‘AAA’ credit rating from Standard & Poor’s.

J&J’s brand leadership and consistent profitability helped the company weather the Great Recession successfully. Here’s his earnings per share during the Great Recession:

- Earnings per share of $4.15 in 2007

- Earnings per share of $4.57 in 2008, up 10%

- 2009 earnings per share of $4.63, up 1%

- 2010 earnings per share of $4.76, up 3%

As you can see, the company increased its profits each recession year. This has allowed us to continue to increase our dividend each year, even as the United States is experiencing a sharp recession. J&J also maintained high profitability and increased its dividend again in 2020, when the global economy was severely impacted by the coronavirus pandemic.

Investors can be reasonably confident that the company will continue to increase its dividend each year.

Valuation and Expected Return

Johnson & Johnson shares are undervalued today. The company expects 2023 adjusted earnings per share to be $10.55. Using the current stock price of $165, the expected return on the stock is 15.4. The estimated fair value of J&J shares is a P/E ratio of 17, meaning the shares are slightly undervalued. An increase in the P/E multiple from 15.4 to 17 could increase annual returns by 2.1% over the next five years.

Future returns, on the other hand, are driven by earnings growth and dividends. The company expects to grow EPS by 6% annually through 2028.

Additionally, Johnson & Johnson has the longest streak of dividends in the market and continues to increase its dividend each year. In April 2022, the company extended its dividend to 60 years in a row after raising his dividend by 6.6%. The stock yields 2.8% today.

Below is a projection of expected total annual returns through 2024.

- 6% increase in earnings per share

- 2.1% multiple return

- 2.8% dividend yield

J&J expects to be able to generate an annualized total return of 10.9% over the next five years. This is a satisfactory level of return for risk-averse income investors.

final thoughts

J&J has increased its dividend for 60 consecutive years. Few things are certain in the stock market, but one of them is that J&J increases its dividend every year. The company has a lot of future growth thanks to its strong pipeline and recent acquisitions.

J&J is attractively valued for its long-term growth prospects and above-market dividends. It should have little trouble raising its dividend each year for years to come. The result is a quality dividend growth stock to buy and hold for the long term.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe.

If you’re looking for stocks with unique dividend characteristics, consider the Sure Dividend database below.

Thank you for reading this article. Send any feedback, corrections, or questions to support@suredividend.com.