(Bloomberg) — Equity markets continue to rise amid optimism about accelerating economic growth and curbing inflation, according to Bank of America’s (NYSE:) latest global fund manager survey. However, most investors are not confident that the rally will continue. .

About 66% of participants in the bank’s February survey said stocks are seeing a bear market rally, indicating they expect a return to new lows. That’s the same even though the share of investors expecting a recession has fallen to 24% from a peak of 77% in November. Pessimism about economic growth hit its lowest point in a year, with 83% of fund managers expecting inflation to ease further over the next 12 months, a survey showed.

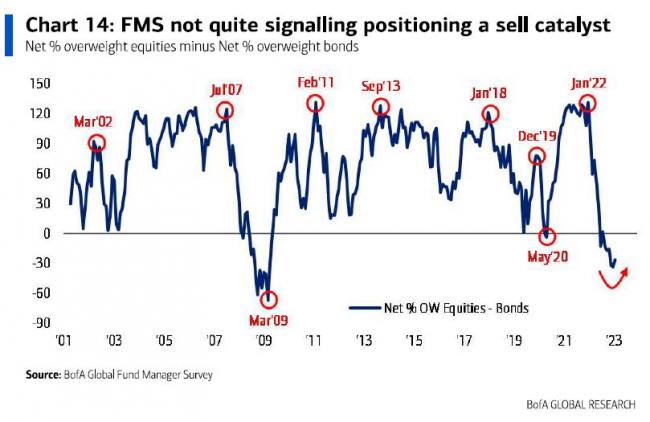

Still, strategist Michael Hartnett said the positioning is still light enough to keep the stock from falling. About 31% of investors are now underweight stocks compared to his peak of 52% in September, which is still higher than the historical average. Meanwhile, Hartnett said cash allocations eased this month and are now at levels just before the start of the war in Ukraine last February.

After a bear market last year, U.S. and European equities have rallied in 2023. Signs of easing inflation have fueled bets that central banks will ease rate hikes. Optimism about economic reopening in China and falling natural gas prices in Europe are also boosting investor sentiment. Still, some strategists, including JPMorgan Chase & Co.’s Marco Kolanovic, remain cautious about the stock’s outlook, saying it still doesn’t reflect the likelihood of a recession.

Read more: JPMorgan’s Kolanovic Urges Investors to Ditch Stocks and Buy Bonds

Hartnett, which was widely dismissive of the stock in 2022, last week recommended selling above 4,200 points, about 1.5% above the final closing price. Equities face their next big test today as US inflation data provides clues to the Federal Reserve’s policy outlook.

A Bank of America survey of 262 fund managers managing $763 billion, conducted Feb. 2 to Feb. 9, finds earnings expectations improving but still bearish. was shown.

Participants still see stagflation as the most likely macro backdrop, with 83% expecting below-trend growth and above-trend inflation in the next 12 months.

Other highlights include:

- The biggest tail risks are persistently high inflation, geopolitical deterioration, a deep global recession, resolutely hawkish central banks, and systemic credit events.

- Some 68% of participants expect China’s reopening to affect inflation

- Exposure to Emerging Markets Equities Soars, Record Three-Month Allocation Growth

- Investors Underweight Defensive Against Cyclicals for First Time Since April

- Most Busy Trades: Long China Stocks, Long IG Bonds, Long USD, Long US Treasuries, Long ESG Assets, Long Oil, Long Emerging Markets Bonds