Updated by Nikolaos Sismanis on March 4, 2023

The renewable energy industry is not widely known as a recession-proof business. Companies in this sector tend to be unprofitable and typically do not pay dividends to shareholders.

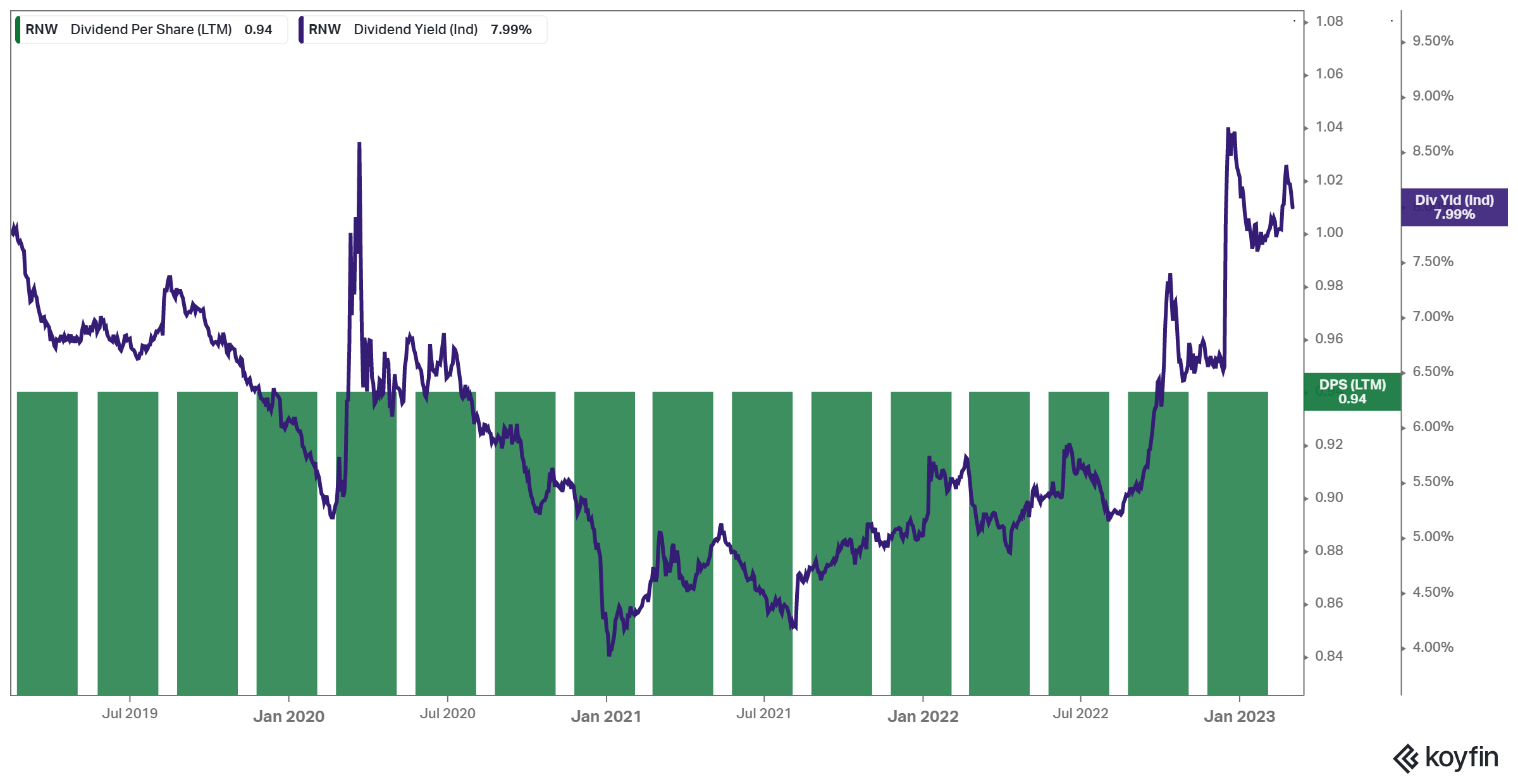

As a result, many investors may avoid the renewable energy industry, but TransAlta Renewables (TRSWF) is an undervalued company in renewable energy. TransAlta is attractive to dividend growth investors for many reasons. First, the dividend yield is as high as 8.0%.

TransAlta Renewables is unique not only in its high dividend yield, but also in that it pays out monthly instead of the traditional quarterly distribution schedule.

Click the link below to download the full list of 69 monthly dividend stocks (and related financial metrics such as dividend yield and payout ratio).

TransAlta Renewables’ high dividend yield and monthly dividend payments are two of the main reasons the company stands out to income investors.

That said, proper due diligence is still required to ensure that high-yield stock payouts are sustainable.

Business overview

TransAlta Renewables is a renewable energy infrastructure company headquartered in Calgary, Alberta.

With a market capitalization of $2.3 billion, TransAlta is Canada’s largest wind energy producer and one of the nation’s largest renewable energy producers overall. The stock is listed in New York and Toronto.

The company’s history in renewable energy generation dates back over 100 years. The company spun off in 2013 from his major shareholder in the alternative power generation company, TransAlta.

The company has maintained or increased its dividend at an average annual growth rate of 2.5% since 2014. TransAlta Renewables owns or has economic interest in 26 wind farms, 11 hydroelectric farms, 8 natural gas farms, 2 solar farms, 1 natural gas pipeline and 1 battery storage project. I have

TransAlta aims for long-term growth by focusing on renewable energy and gas-fired power generation. As such, most countries are benefiting from the long-term transformation of moving from fossil fuels to clean energy sources. Even better, this change has accelerated significantly since the outbreak of the pandemic.

TransAlta generates strong cash internally and can be invested strategically to build its portfolio. These investments provide the company with positive growth prospects.

growth outlook

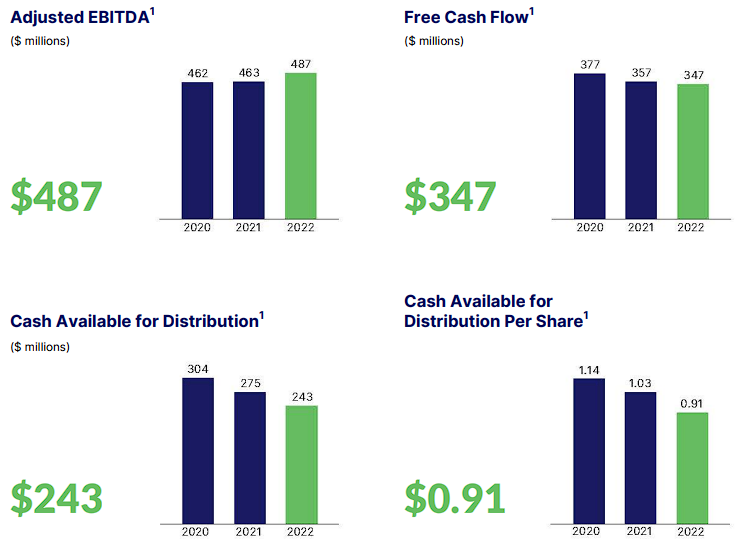

TransAlta’s track record of growth is very strong. The company has consistently increased its production capacity over the past few years thanks to investments in wind, solar and hydropower assets. That said, rising interest rates and increasingly expensive equity issuance are taking a toll on the company’s distributable cash and his CAfD per share.

Source: Annual Report

Overall, it’s clear that TransAlta has invested heavily in its growth projects, given its $2.3 billion market capitalization.

TransAlta has also proven resilient through the coronavirus crisis. In contrast to most oil companies, which suffered heavy losses in 2020 due to the collapse in global demand for petroleum products, TransAlta has increased its earnings per share from $1.13 in 2019 to $0.99 in 2020. of funds under management decreased by 12% (in US dollars, as with all figures presented in this article).

The company made a partial recovery in 2021, increasing its funds under management from $0.99 to $1.05 per share. But now it faces an unexpected headwind as towers collapse at the Kent Hills 1 and 2 wind sites.

After a careful inspection of the sites, the company determined that both sites required replacement of the entire foundation. This he plans to complete by the end of 2023. The exchange will cost him $75 million to $100 million. On the bright side, recent progress in deleveraging should help reduce the interest burden and boost the CAfD.

In addition, TransAlta has promising growth prospects in the long term thanks to the long-term growth of clean energy sources. Organic growth is not only an acquisition, but a catalyst for the future. In 2021, the company acquired several renewable energy plants. In 2022, there were no acquisitions due to higher funding costs, but we expect acquisitions to resume once the company deleverages further and frees up some room for further debt issuance. .

On the other hand, TransAlta’s results have been somewhat volatile, largely due to unpredictable asset depreciation as a result of overinvestment.

Additionally, the issuance of new shares used to fund the company’s overinvestment created headwinds to earnings growth. Given that the stock is trading at huge yields, we hope TransAlta does not issue additional stock at this time. As a result, over the next five years, he expects AUM per share to grow by an average of 1% annually.

Dividend analysis

TransAlta Renewables’ dividend is clearly a big draw for investors, given its very high yield. Additionally, this isn’t necessarily a growth company, so the total return will depend heavily on dividends over the next few years.

The company’s dividend has grown to 2.5% compounded annually since its IPO in 2013, and is now at $0.94 per Canadian dollar per share annually. Converted to US dollars, the annual dividend payout is about $0.70 per share for him, giving a dividend yield of 8%.

Note: Because it is a Canadian stock, US investors investing in the company outside of a retirement account are subject to a 15% dividend tax. A guide to Canadian taxes for US investors can be found here.

TransAlta’s share price has recovered in 2021 from a general marker selloff caused by the previous year’s COVID-19 pandemic, but has again fallen to a multi-year low. This is likely due to investors questioning the company’s ability to grow in the current environment. Because the cost of issuing debt and equity is enormous.

Rising interest rates will put pressure on a company’s CaFD and could even threaten a dividend if the company doesn’t deleverage quickly enough. Still, the company expects to keep paying for now. The payout ratio on earnings in 2018 was 71% or 82% using distributable cash. Using distributable cash yielded payout rates of 66% in 2021 and 75% in 2022.

With this in mind, we believe payments are safe for the time being. There may even be room for continued dividend growth if the company’s future investments increase per his share.

final thoughts

TransAlta Renewables’ high dividend yield and monthly dividend payout are immediately attractive to income investors such as retirees. However, maintaining such a high dividend yield requires due diligence.

This analysis suggests that the company’s dividend is relatively safe. It is measured by cash available for distribution or working capital. Investors looking for monthly dividends from the renewable energy industry can do well with owning TransAlta Renewables, but they also emphasize that dividends should not be blindly trusted.

If the company chooses to pursue costly financing to support its growth, we cannot rule out the possibility that a dividend cut will be considered.

If you’re looking to find more quality dividend growth stocks for your long-term investment, the Sure Dividend database is here to help.

Major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles and updates the following stock market databases monthly.

Thank you for reading this article. Send any feedback, corrections, or questions to support@suredividend.com.